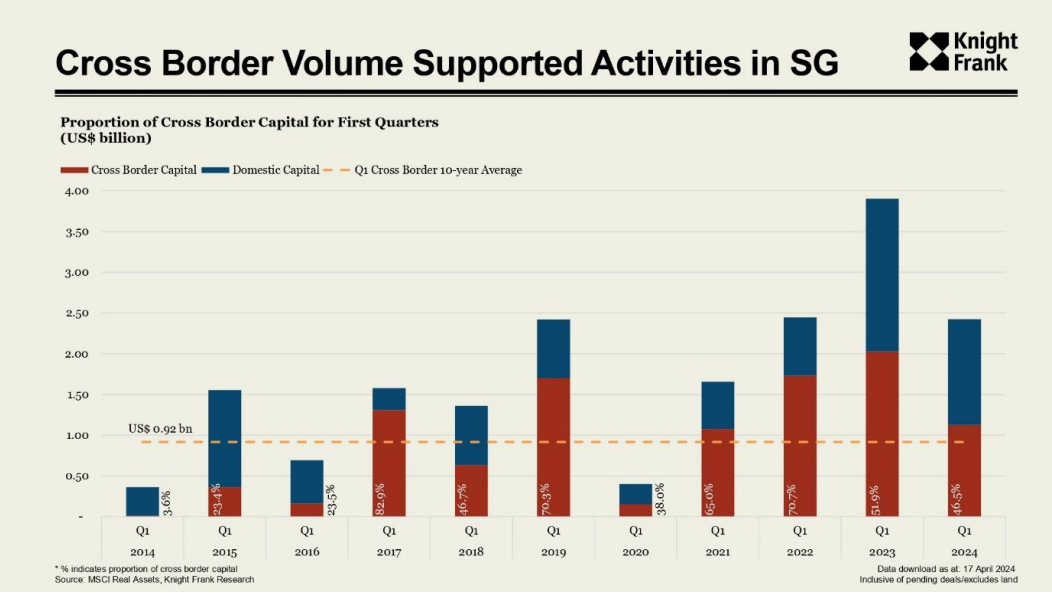

Cross-border investment in Singapore strengthened significantly in the first quarter of 2024, rising 22.8% above the 10-year average, according to an analysis by Knight Frank’s Asia-Pacific research team. Cross-border capital supported overall investment market activity, with Singapore receiving the highest proportion (45.6%) of overseas capital among Asia-Pacific markets during the quarter.

Institutional investors played a significant role, accounting for six of the 11 buyers and contributing US$906 million in transactions. This group's strong demand in the hospitality sector was a key driver of the growth. The resurgence of the tourism industry and heightened acquisition activity in Singapore's hospitality market further stimulated investors' interest in hospitality assets.

Christine Li, Head of Research, Asia-Pacific at Knight Frank said, “Our research shows that in the face of a 29% quarter-on-quarter decline in cross-border activities across Asia Pacific, Singapore bucked this trend. The hospitality sector attracted significant interest from institutional investors with its optimistic outlook and improving operational metrics. The market is ripe for increased investment activity, as investors are particularly drawn to value-added opportunities, signalling potential growth and development within this sector.”

The MICE (meetings, incentives, conventions, and exhibitions) sector, coupled with government initiatives such as the China-Singapore 30-Day Mutual Visa Exemption, have been instrumental in driving tourism demand.

South Korea and Japan power office investment resurgence While the overall trend in cross-border investment volumes across Asia-Pacific experiences a downturn, South Korea and Japan have attracted renewed commercial investment interest, particularly in the office sector.

In South Korea, investment volume reached US$ 5.8 billion with a 12.5% quarter-on-quarter rise and 180% year-on-year increase compared with Q1 2023.

Office deals dominated the market, accounting for 64.7% of the total investment volume – with a 69.6% quarter-on-quarter rise and a six-fold year-on-year increase

Shift from self-occupancy acquisitions by strategic investors to increased office investments by Korean institutional investors

Hospitality assets attracted US$ 850 million in investment, marking a 234.7% increase from Q4 2023 and a 44-fold year-on-year expansion, primarily funded by institutional investors

Neil Brookes, global head of capital markets at Knight Frank said, “The re-emergence of domestic institutional investors signals their potential role in shaping the market's future. However, their influence may be tempered by the challenge of negative leverage. Simultaneously, foreign investors are maintaining a cautious approach, awaiting price adjustments before actively pursuing transactions. Discrepancies in pricing expectations between buyers and sellers could delay deal closures, further affecting market activity. This trend will likely continue until substantial interest rate and liquidity improvements become evident. “

Despite an overall contraction in real estate investment volume, with a 13.2% quarter-onquarter and 28.3% year-on-year decline, Japan is witnessing renewed investor interest in office and industrial assets.

Office transactions accounted for almost half of the total volume, which doubled from the previous quarter but dropped 31.6% year-on-year

Investors are motivated by the positive momentum anticipated for the office sector, underpinned by consistent occupier demand

Yield-chasing industrial sector ranked second at 27.4% of volume, driven by a US$ 694 million logistics portfolio deal

Despite the Bank of Japan's recent decision to raise short-term interest rates to 0-0.1% in March 2024, the overall investment climate is not expected to change drastically, and a steady capital inflow into the real estate sector is anticipated to continue. However, if long-term interest rates experience further hikes, investors might demand higher capitalisation rates in sectors such as office, facing stagnant market rents. This could lead to a widening gap between sellers' asking prices and buyers' offers, potentially hindering transaction volume and affecting overall market liquidity.

The shift in Japan's monetary policy could also impact exchange rates, with fluctuations in the Japanese Yen's value possibly encouraging cross-border investments as assets become more affordable in investors' home currencies. As a result, strategic partnerships and targeted investment approaches will be critical in capitalising on market opportunities.”